For years, flower was the centerpiece of cannabis retail. It dominated dispensary menus, consumer spending and the culture surrounding industry. But in 2025, that hierarchy changed.

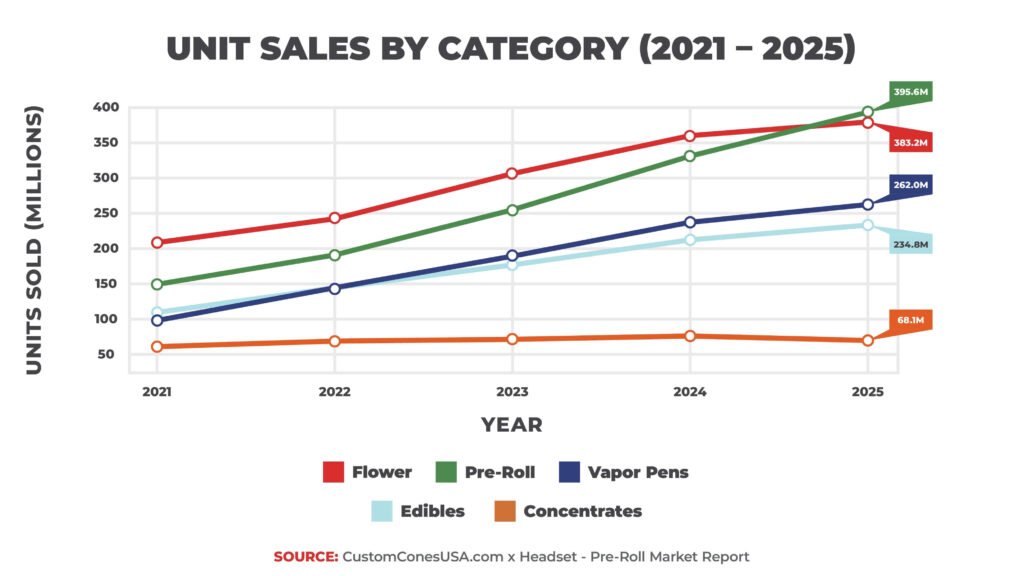

According to the 2026 State of the Pre-Roll Market Report by Custom Cones USA, pre-rolls overtook flower in unit sales for the first time, becoming the top-selling cannabis product on the market by volume. Category revenue rose 9.8% year-over-year to nearly $3.6 billion, while unit sales jumped 18.6% to 383.2 million units sold.

It was one of the most significant product shifts the industry has seen since legalization began. But while pre-roll growth was national, one state stood above the rest when it came to momentum: New York.

The Empire State posted the fastest pre-roll growth in the country in 2025, signaling that one of America’s largest consumer markets is still in the early innings of cannabis expansion.

The report found New York generated $330.6 million in pre-roll sales in 2025, placing it fourth nationally in total revenue despite a relatively young adult-use market. More impressively, the state posted a staggering 96% increase in revenue year-over-year, along with a 120.4% increase in units sold, and no other tracked market came close.

For context, many mature cannabis states are now seeing modest single-digit gains, flat performance or outright declines in some categories. New York nearly doubled. That type of acceleration suggests the state is still ramping, with consumer demand continuing to outpace market saturation. (INSERT GRAPH HERE)

Why New York Matters So Much

New York is not just another legal state, it is one of the largest and most influential consumer markets in the world.

With a population of roughly 20 million residents, dense urban centers, global tourism and cultural influence that reaches far beyond state lines, New York has long been viewed as a potential heavyweight in cannabis.

The slow rollout of adult-use licensing initially tempered expectations, but the 2025 data suggests the market is now entering a stronger growth phase.

For brands, investors and operators, that matters because when New York scales, it can materially impact national cannabis trends.

The rapid rise of pre-rolls in New York is not surprising when viewed through a consumer behavior lens. Pre-rolls are one of the most accessible cannabis formats available, no grinder or rolling skill needed, lower upfront cost than larger flower purchases and convenient for social settings or quick sessions.

Those benefits can resonate strongly in dense metro environments where space, convenience and simplicity matter. In cities where consumers may not want to store jars of flower or extra accessories, pre-rolls offer a plug-and-play option. That likely gives the category an advantage in markets like New York City and surrounding metro areas.

The report found New York’s average pre-roll price was $20.47, one of the highest in the country, compared to Michigan at $4.58, Washington State at $6.50, Oregon at $7.52 and Colorado at $8.40. Higher pricing can reflect multiple factors including supply constraints in newer markets, premium brand positioning and urban operating costs. While lower prices often come later as markets mature, New York’s current pricing structure shows consumers are still buying heavily even at elevated rates; a strong demand signal.

See also: Call Log Verification – Cyberpúerta, Drrodrigoharo, vittenthill49, heimvinec6025, elldlayen854

New York Is Already Among the Leaders

Despite being newer than legacy markets like California, Colorado, Oregon and Washington, New York already ranked #4 nationally in pre-roll revenue, among the top states in market share, and is the clear leader in annual growth. Usually, young markets grow fast from a small base, but New York is growing fast while already generating hundreds of millions in category sales, indicating the market’s ceiling has yet to be reached.

New York was not alone. The report also noted strong gains in nearby states New Jersey, which saw revenue up 50.5% and units up 79.2%, and Connecticut who ranked third in unit sales growth. Observed together, the data points to a rising Mid-Atlantic corridor where cannabis adoption, and especially pre-roll adoption, is accelerating.

That regional growth could benefit brands able to establish recognition across multiple neighboring markets.

For operators watching the national landscape, New York may represent one of the most important near-term opportunities because it combines massive population and cultural influence with room to grow in a category fit for the urban consumer. In short, New York offers both scale and upside.

What Comes Next

The report projects continued national pre-roll growth in 2026, with total category sales expected to reach between $3.8 billion and $4 billion. It specifically highlighted New York, New Jersey and Connecticut as key expansion regions moving forward.

If that forecast proves correct, New York may move from the fastest-growing market to one of the dominant markets in cannabis. But the larger message is clear: pre-rolls overtook flower because consumer preferences are changing nationwide.

New York’s explosive rise shows those changes may be strongest in markets that are only just beginning to mature. Flower may still carry legacy status, but in America’s biggest emerging cannabis market, pre-rolls are setting the pace.